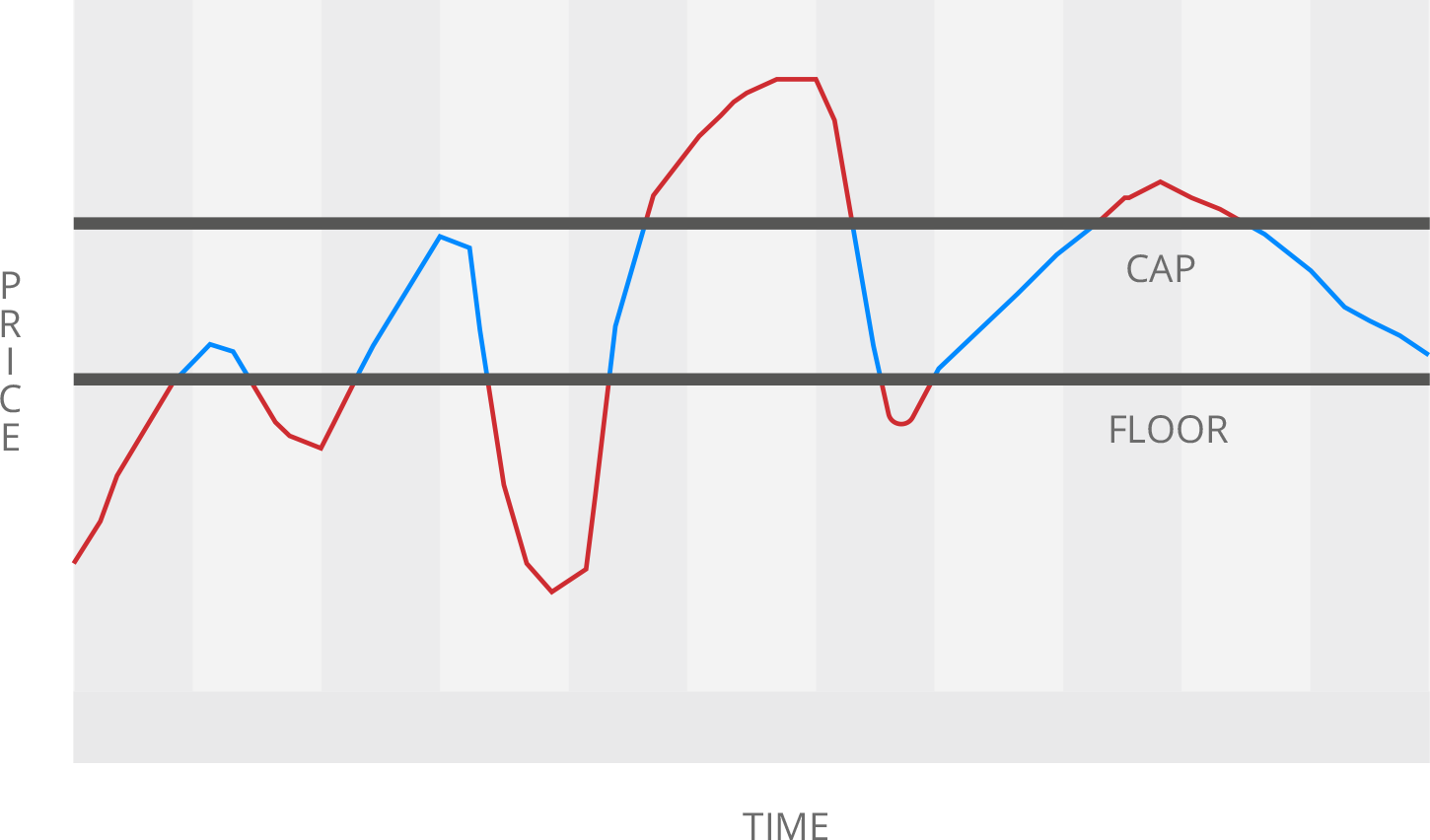

Collars And Price Floors Caps

Calpine Energy Solutions Products Price Collars

Http Janroman Dhis Org Stud Ii2008 Caps And Floors Pdf

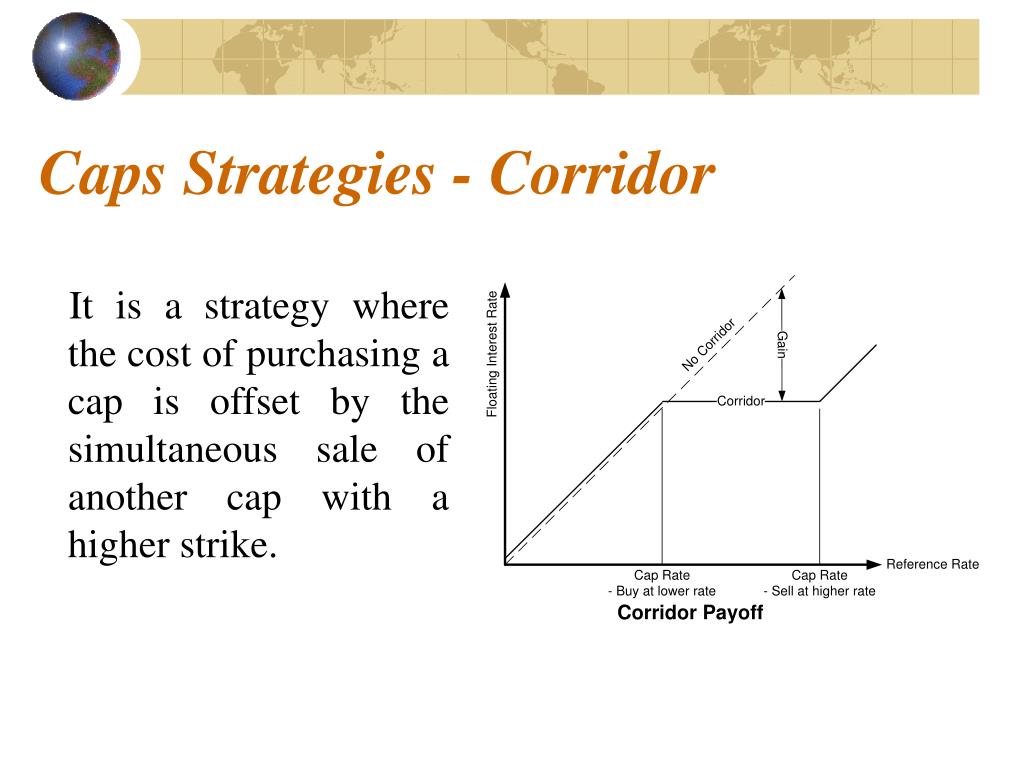

Ppt Caps Floors And Collars Powerpoint Presentation Free Download Id 6803699

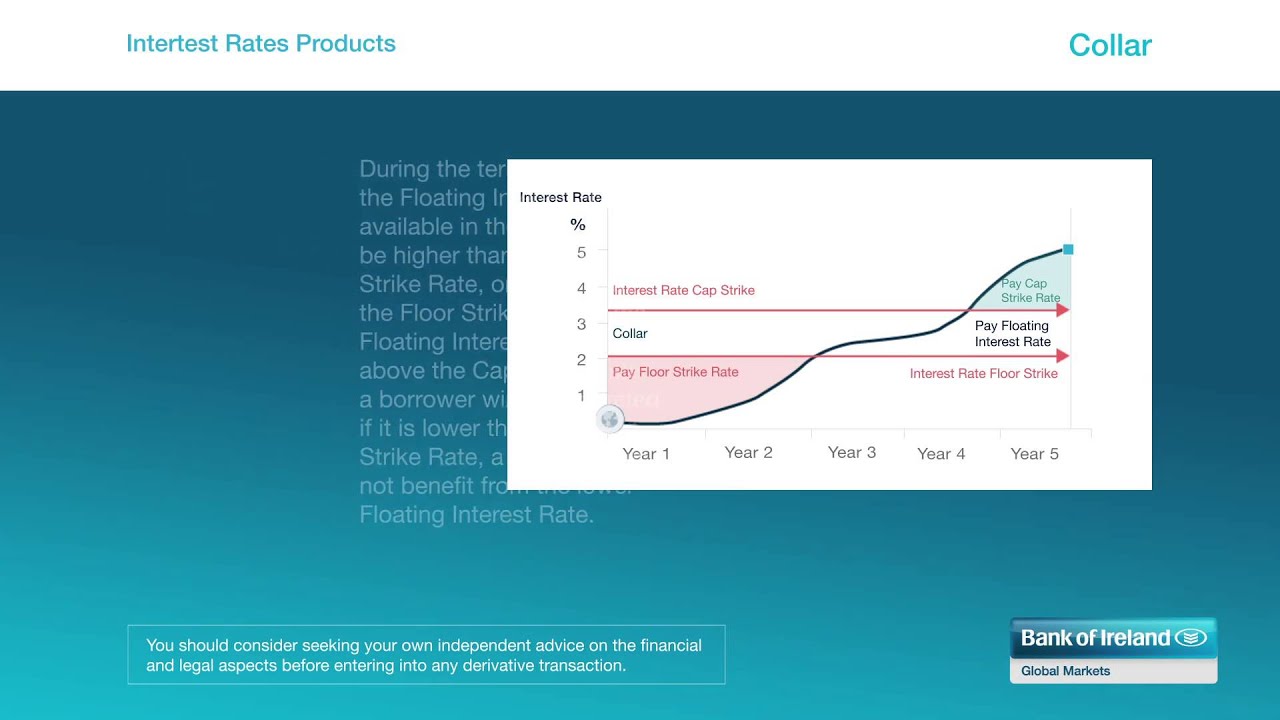

Interest Rate Products Caps Collars Youtube

:max_bytes(150000):strip_icc()/strategy-4086857_19201-23485cf7c4bf4dbbb95c93f267285f16.jpg)

Interest Rate Collar Definition

Multi Period Options Interest Rate Caps Interest Rate Floors Ppt Video Online Download

These latter two are a short risk reversal position.

Collars and price floors caps.

Rate Cap Swap And Collar A Cheat Sheet To Managing Rate Risk Derivative Logic

Houston Astros Personalized Classic Leather Baseball Collar Leather Dog Collars Classic Leather Leather Collar

Make Your Own Dog Collar I Have Been Wanting A Bowtie Collar For Dexter But They Are So Expensive Dog Collars Leashes Diy Dog Collar Dog Leash

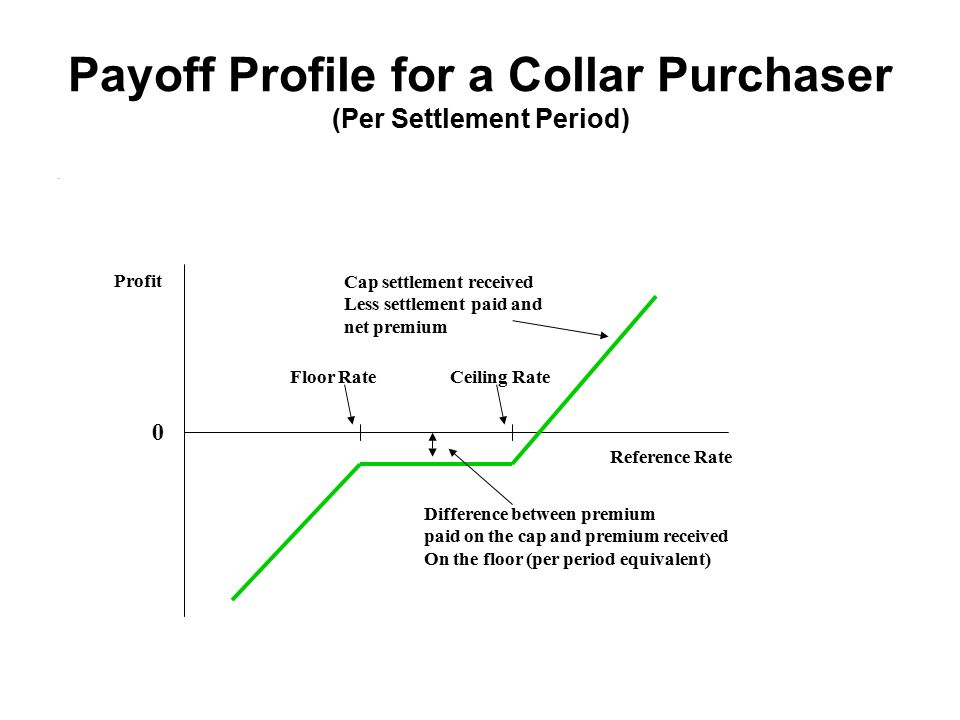

Caps Floors And Collars Ppt Download

Source : pinterest.com